.png)

Bitcoin stands alone as the top performing asset since it was created over 17 years ago, continually delivering extraordinary results for people who hold it across multi-year durations. Investors and institutions of all levels have taken notice, up to the highest peaks of finance and government. When bitcoin ETFs were finally approved to trade on the U.S. stock market in January 2024, it led to some of the most successful ETF launches of all time.

Now that people can buy these ETFs tracking the spot price of bitcoin within their brokerage account alongside other equities, the extra hurdles associated with buying bitcoin (such as signing up with a separate crypto exchange) have been removed—at first glance. However, few understand the full consequences of this approach until it’s too late. In this article, we’ll discuss the costly downsides of bitcoin ETFs that are important to be aware of.

A recap of how bitcoin is stored and controlled

Bitcoin doesn't exist in a physical form the way cash or gold does. Instead, every bitcoin balance is recorded on a global digital ledger called the blockchain, maintained simultaneously across thousands of computers worldwide. What can be physically held, however, are bitcoin keys that grant access to a bitcoin balance. You can think of it like a password that unlocks a safe deposit box that exists everywhere and nowhere at once. Whoever holds the keys controls the bitcoin.

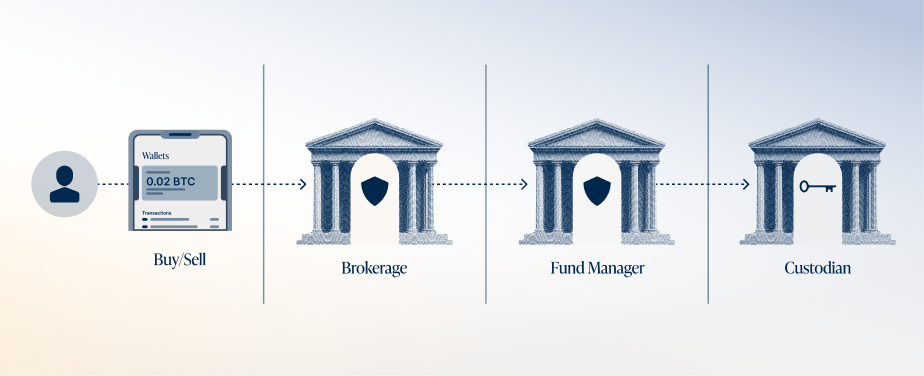

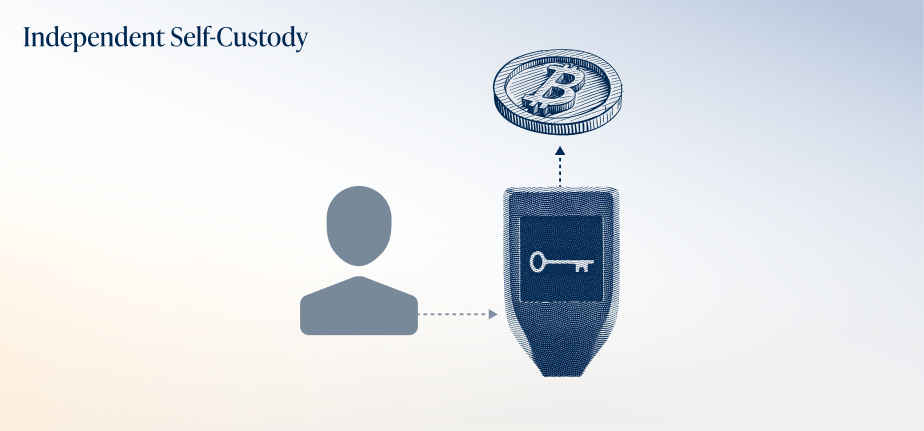

Because control over bitcoin comes down to who holds these keys, the question of ownership is really a question of custody. If you want to own bitcoin, you must choose to either control it yourself by holding your own keys, or by trusting someone else—a custodian—to hold keys on your behalf. Trusting a third-party custodian is the model attached to using a bitcoin ETF, and it introduces several layers of counterparties and limitations.

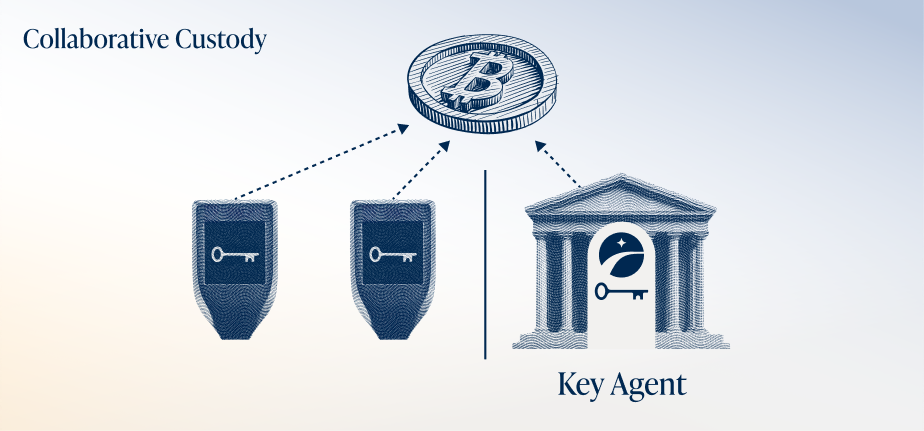

If you choose to self-custody bitcoin by holding your own keys, you can achieve direct access to your bitcoin, and independence from third-party custodians. Another middle ground option is collaborative custody, which also provides you with independent access to your bitcoin, alongside backups and support from institutional experts. We’ve compared all of these approaches to bitcoin ownership in a dedicated article.

How a bitcoin ETF can trap you

Owning an ETF which represents a commodity like oil, gold or bitcoin is a lot like owning an “IOU” certificate more than owning the commodity itself. You can’t power your car with an oil ETF or make jewelry out of a gold ETF. Similarly, if you have a bitcoin ETF you’re unable to obtain the full benefits of owning actual bitcoin, which we will discuss further in the next section.

If you hold a bitcoin ETF and later decide you want to hold real bitcoin instead, there are several significant obstacles that could get in your way. Although bitcoin ETFs have explored in-kind redemptions—the ability to directly redeem the ETF shares for the underlying bitcoin—these are only available for authorized participants, or large institutional market-makers. Individual retail investors can’t redeem their shares for bitcoin, and must instead sell the ETF shares to get cash before finally buying bitcoin separately. This might mean transferring the cash through the banking system to a different financial institution that offers bitcoin trading, a process that could be extra stressful, especially if the price of bitcoin is moving up rapidly.

Beyond the procedural friction of converting a bitcoin ETF to real bitcoin, there is a potentially far costlier obstacle waiting for investors who have held through any significant price appreciation: capital gains tax. If you sell a bitcoin ETF at a higher price than when you bought it, you may be subject to capital gains tax. If you’ve held the ETF for a while, and bitcoin has maintained its trend of delivering exceptional returns, then the potential tax implications can be enormous. For most Americans, selling a bitcoin ETF after significant long-term price gains could mean losing up to 15-20% of your holdings.

Federal long-term capital gains rates shown; state taxes and the Net Investment Income Tax may apply. Your rate depends on income, holding period, and state of residence.

For investors who think they may ever want to hold real bitcoin, the time to consider migrating away from an ETF is before gains accumulate, not after. If a migration is on the table, a period of price weakness can also reduce (or eliminate entirely!) the capital gains bill, making downturns a strategically critical window to take action.

4 reasons for choosing bitcoin over a bitcoin ETF

Owning real bitcoin rather than a bitcoin ETF has several advantages. ETFs limit when you can act, introduce ongoing fees, restrict how you can use your bitcoin, and add layers of counterparty risk that don’t exist with direct ownership. Let’s take a closer look at each of these.

1: Limited hours of availability

The U.S. stock market is only open for about 20% of the hours in a week, while bitcoin itself is one of the world’s most liquid assets and trades 24/7/365 in all global markets. While Wall Street is gearing up to move to more flexible hours in the years ahead, the current limitations can lead to some recurring uncomfortable situations among bitcoin ETF users. When bitcoin moves dramatically outside of market hours, its price could temporarily hit values you’ve identified as targets for buying or selling, while the stock market is unable to accommodate your intention.

During a normal two day weekend, the stock market is closed for roughly 65 hours straight. On holiday weekends the market could be closed up for up to nearly 90 hours straight, or 3.73 days. Because bitcoin is notorious for occasions of intense volatility, these periods could feel like a very long time to be locked out of participation. Huge opportunities can present themselves without a way to take full advantage of them if you limit yourself to ETFs in a brokerage account.

2: ETF annual fees

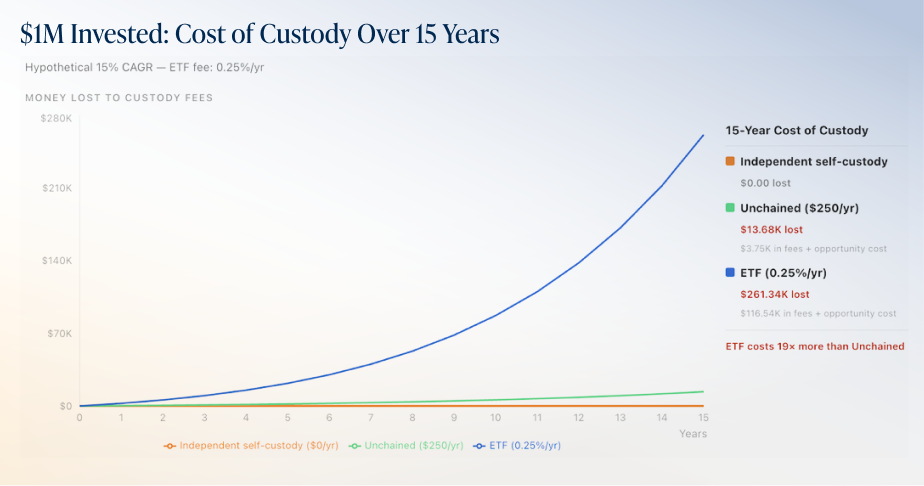

Most ETFs charge an annual fee, which is how the fund makes a profit. Bitcoin ETFs are no exception—among the 5 largest bitcoin ETFs, the median annual fee is 0.25%. That may not seem like much, but as it compounds across time, the total fees taken can become a serious issue (especially in the context of substantial bitcoin holdings, which a modest investment could eventually become).

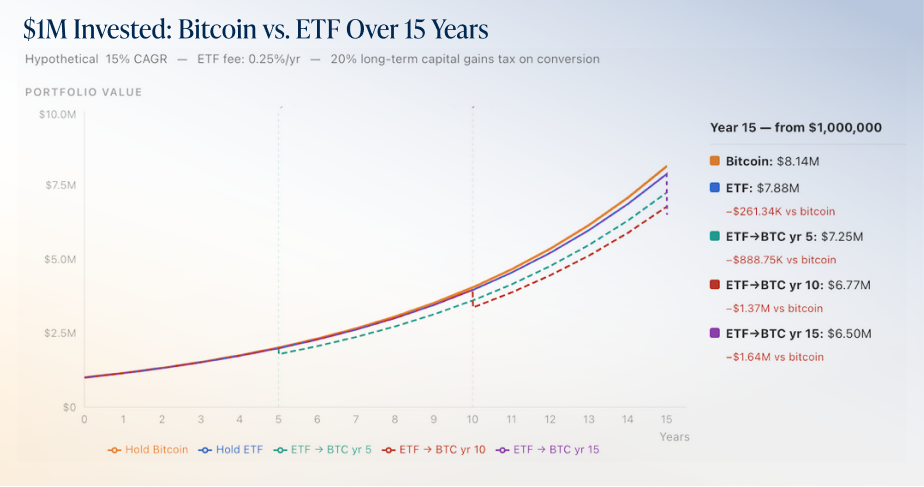

For example, suppose bitcoin has a 15% cumulative annual growth rate (CAGR) for the next 15 years, which is very conservative based on bitcoin’s historical growth. A $1M investment in real bitcoin would grow to $8.14M, but an ETF charging 0.25% annually would extract $261k in fees during this span! Further fees would continue to be extracted indefinitely until the ETF is sold, which could also trigger hefty capital gains taxes.

You can avoid the compounding extraction of annual fees by holding bitcoin itself, which has no ongoing costs beyond optional security and inheritance strategies. For example, an Unchained vault has a flat fee of $250 per year regardless of the amount of bitcoin held, translating to under $4k in fees during our hypothetical 15 year span, rather than the $261k of a bitcoin ETF.

Many people hesitate to escape ETF annual fees because they don’t want to incur a capital gains tax burden, but this only makes matters worse down the road. The longer you wait to switch from an ETF to real bitcoin, the more fees will be extracted and the more capital gains are incurred (assuming bitcoin continues to appreciate).

ETF fees are subject to change

There is also evidence that the ETFs providers are aware of their customers’ hesitation to exit their position, and can use it to their advantage. One of the three biggest bitcoin ETFs, Grayscale’s GBTC, charges a much higher annual fee than the others at 1.50%. Their product existed before the other bitcoin ETFs as a closed-end bitcoin trust, which was then converted into an ETF in 2024. Presumably, a major reason why holders of GBTC haven’t switched to a different ETF with much lower fees is because they want to avoid the capital gains tax. It’s possible for other bitcoin ETF providers to follow a similar strategy in the future, by raising fees once bitcoin undergoes major appreciation. The 0.25% fees most bitcoin ETFs charge today aren’t set in stone for the years to come.

3: Participation in the bitcoin economy of transfers

Part of what makes bitcoin special is its ability to be transferred between any two people worldwide within minutes, and without relying on a centralized intermediary. This feature can help people overcome financial censorship, as well as tedious and expensive international transfer processes. Until bitcoin, the global movement of money had never been able to achieve such a combination of freedom and speed.

However, these unique attributes can’t be utilized by holders of a bitcoin ETF. Transferring an ETF from one specific person to another is an uncommon process (such as in the context of a gift or inheritance) that is neither instantaneous, nor global, nor permissionless. Even if two people have accounts at the same brokerage, a transfer can require special paperwork and several business days. Two people using different U.S. brokerages would involve deeper financial infrastructure provided by the monopolistic Depository Trust & Clearing Corporation (or DTCC), and this could take additional business days to complete. If the two people are in completely different countries using international brokerages, a direct transfer is often impossible, or could take weeks.

The number of merchants in the US that accept bitcoin is large and growing every day, and spot bitcoin held directly, unlike an ETF, can easily be moved between wallets if you’re interested in experimenting with buying coffee or lunch with bitcoin.

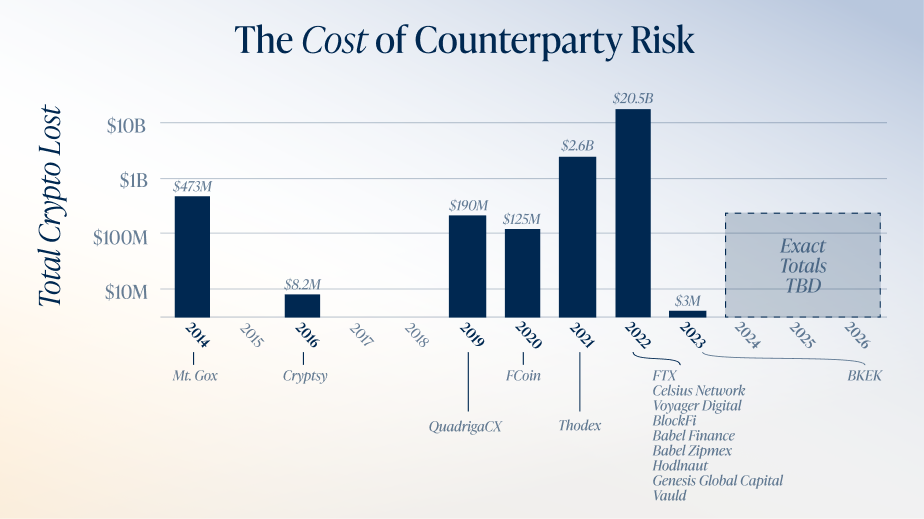

4: Counterparty risk

Bitcoin was launched in 2009, shortly after the global financial crisis. This historical backdrop fueled critiques of the existing financial system and the trust required to make it work, which can be found in the bitcoin whitepaper itself. Bitcoin introduced a new, alternative system that minimizes trust and uncertainty. However, since then we’ve witnessed a pattern of people choosing to reintroduce trust by letting a custodian hold their bitcoin, eventually ending in fractional reserves and catastrophe. Examples include Mt. Gox in 2014, then QuadrigaCX in 2019, then FTX, BlockFi and Celsius in 2022. Bitcoin has a strict finite supply and no bailouts, so if custodians take risks or fail to protect bitcoin from loss or theft, recovery is often impossible.

When using a bitcoin ETF, there are several layers of trusted third parties that could be a risk to your funds. First is the custodian in charge of holding and securing the bitcoin—most of the ETFs currently use Coinbase Custody Trust Company, while Fidelity’s FBTC uses Fidelity Digital Asset Services, LLC. These entities could be targeted by hackers or suffer losses through operational failures, as has happened in the past. Second is the ETF provider, or sponsor, which includes names like BlackRock, Fidelity, Grayscale, and ARK. These managers can make decisions such as changing the annual fees of their ETFs, or if bitcoin ever split into two coins due to a hardfork, the sponsor generally gets to choose which coin is the “real” bitcoin for their customers (each ETF has its own unique legal language on this issue which can be investigated). Third is your brokerage, the service you use to buy and hold ETF shares, such as Vanguard, Charles Schwab, or Fidelity Investments. If a brokerage becomes insolvent, SIPC insurance covers up to $500k in securities, with a $250,000 cash sublimit, but reimbursement can take considerable time, may be paid in cash rather than ETF shares, and could be valued at a price from before the payout date rather than the current market value.

Is holding real bitcoin better than a bitcoin ETF?

Given the reasons listed above, it’s clear that holding real bitcoin gives you more flexibility at a lower cost when compared to a bitcoin ETF. It can also be the more secure option if counterparty risks ever materialize, as they repeatedly have in the past.

That said, attempting to self-custody bitcoin without a solid understanding of the risks and technology involved can lead to serious mistakes, including permanent loss of funds. This can make an ETF the more pragmatic choice for some people in the short term, while building bitcoin knowledge. We cover this point in an article dedicated to comparing the spectrum of approaches to bitcoin ownership.

For many people, self-custody with proper support may be a better decision rather than going it alone. If you have access to expert support, the common pitfalls around keys, custody, and inheritance planning become navigable, and you can still retain full control of your bitcoin. This is the foundation of Unchained's collaborative custody model. If you're considering making the transition from a bitcoin ETF, speaking with our team on a free consultation is a great place to start and ask questions. As discussed,it can be useful to evaluate the decision against your current cost basis, particularly during periods when bitcoin's price has pulled back from its highs.

Even IRAs and 401ks can escape the ETFs

If you hold a bitcoin ETF in a tax-advantaged retirement account, you might assume that ETFs are your only option for bitcoin exposure. However, transitioning to an Unchained IRA lets you hold your own keys to real bitcoin. Although Roth IRAs and Roth 401ks don’t incur capital gains taxes, the other benefits of real bitcoin over an ETF still apply. Taking action now can reduce the compounding fees taken by ETFs, allowing for greater tax-advantaged growth over the long-term.

No contents of this article may be relied upon as tax, legal, or financial advice, as they have not been tailored to you and have not been reviewed by any attorney, financial advisor, or tax professional. For any questions related to your own specific situation, please consult with your own attorney, tax professional, and/or licensed financial advisor.

Any hypothetical scenarios, growth rates, tax figures, or fee comparisons are illustrative only. They are not forecasts or recommendations and are based on assumptions stated in the article.

Third-party information in this article including ETF sponsors, custodians, fees, and regulatory framework descriptions is accurate to the best of our knowledge as of April 22, 2026 and may change. Competitor and third-party names are used for factual reference only and do not imply any relationship, endorsement, or allegation of wrongdoing.